A Modern Guide to Investing in Gold

In a world of volatile cryptocurrencies and lightning-fast tech stocks, buying a lump of shiny yellow metal can feel almost archaic. But don't let its ancient appeal fool you. Gold is still a cornerstone of smart investing, a trusted store of value, and one of the best defenses against economic storms. It’s not a museum piece; it’s a living, breathing asset with a track record that speaks for itself.

Why Gold Still Matters in a Modern Portfolio

Seasoned investors don't hold gold expecting it to skyrocket like a hot stock. Instead, they rely on it for a few critical reasons that are as true today as they were a thousand years ago. Think of gold less as an engine for growth and more as a financial seatbelt—your portfolio's insurance policy against the unexpected.

A Powerful Hedge Against Inflation

When the value of paper money like the U.S. dollar starts to drop, the price of gold often goes in the other direction. Why? Because gold has intrinsic value that isn't tied to the decisions of any single government or central bank.

Real-Life Example: Just look at the high-inflation era of the 1970s. As the cost of living soared in the U.S., investors who held gold watched their wealth hold steady, preserving their purchasing power while those holding only cash saw it erode daily.

This classic inverse relationship makes gold a crucial tool for keeping your long-term savings from losing their punch.

A Safe Haven in Times of Turmoil

Markets move in cycles, and sometimes those cycles get ugly. Whether it's a stock market crash, a geopolitical crisis, or a deep recession, investors instinctively run from risky assets and seek shelter. More often than not, they run straight to gold.

This "flight to safety" is a predictable pattern that pushes gold's price up when most other investments are taking a nosedive. The 2008 financial crisis is a perfect example. While stock markets around the world were in freefall, gold's value soared, cushioning the blow for anyone who had it in their portfolio.

The Ultimate Portfolio Diversifier

Here’s where gold really shines. Its price tends to move independently from stocks and bonds, a trait known as low correlation. This is just a fancy way of saying that when your stocks are having a bad year, there’s a good chance your gold is having a good one.

This helps smooth out the wild swings in your portfolio's value over time. If you're looking for more ways to protect your investments, you can learn how to diversify your portfolio effectively in our detailed guide.

Adding a bit of gold isn't just about buying a metal; it's about buying balance. Even a small allocation can lower your overall risk and create more consistent returns, which is the name of the game for any serious long-term investor.

How the Global Gold Market Actually Works

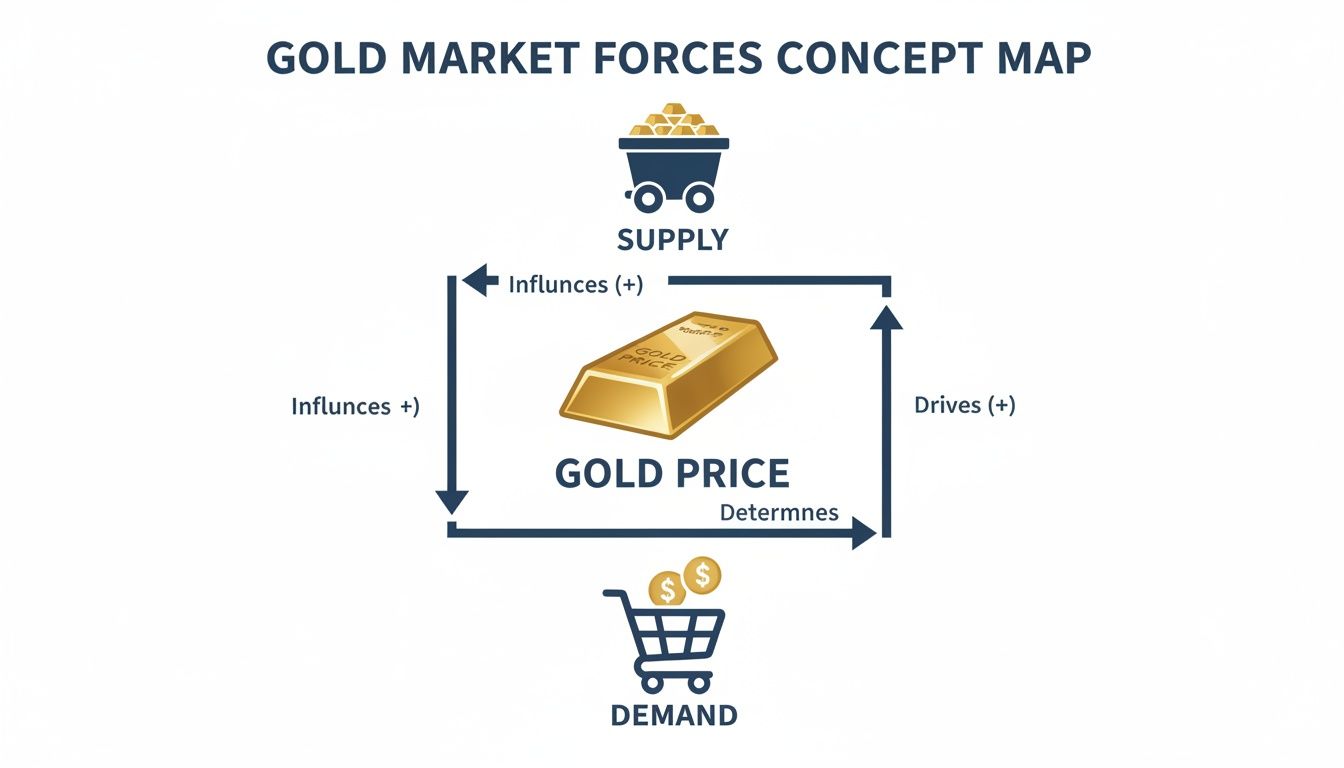

The price of gold isn't pulled out of thin air. It’s the result of a constant, global tug-of-war between supply and demand. Grasping how this marketplace works is the first step to understanding why gold’s value moves the way it does.

On one side, you have all the gold available in the world. On the other, you have everyone who wants to buy it. The tension between these two forces sets the daily "spot price" of gold—that's the number you see scrolling across the bottom of financial news channels.

Let's look at where all this gold comes from and, just as importantly, where it all goes.

The Supply Side: Where Gold Comes From

Gold gets into the market in two main ways: it’s either dug out of the ground or it’s recycled from existing products.

- Mining Production: This is the big one—the primary source of new gold. Global mine production recently hit around 3,300 metric tons in a single year. Countries like China, Russia, and Australia are the heavy hitters, and along with Canada and the United States, they account for a whopping 41% of global output.

- Recycling: A huge amount of gold re-enters the market every year by being melted down and repurposed. Think old jewelry, coins, and even gold salvaged from electronics. This "above-ground" stock is what makes gold so unique. Unlike oil or wheat, nearly every ounce of gold ever mined is still around in some form.

The Demand Side: Who’s Buying All The Gold?

Gold demand is a lot more varied than its supply, with different buyers wanting it for completely different reasons. This mix of motivations is what makes the market so complex and fascinating.

- Jewelry: Believe it or not, jewelry is still the king. This industry soaks up roughly half of the world's annual gold supply. Consumer tastes, especially in massive markets like India and China, have a direct and powerful impact on global demand.

- Investment: This is where you and I come in. Investors buy gold bars, coins, and Exchange-Traded Funds (ETFs) to store wealth and protect their portfolios. When the economy looks shaky, demand from this corner of the market tends to shoot up.

- Central Banks: Don't forget the big players. Governments and their central banks hold immense gold reserves to back their currencies and provide stability. In recent years, they’ve been on a buying spree, adding significant upward pressure on demand.

- Technology: Gold is a fantastic conductor of electricity and doesn't corrode. That makes it a critical component in the electronics we use every day, from the smartphone in your pocket to the computer on your desk. This creates a small but very steady stream of industrial demand.

To really get a feel for the market, it helps to understand the metal itself, including things like the difference between gold karats.

Key Factors That Move the Gold Price

Beyond the basics of supply and demand, a few major economic forces can really push the price of gold around. If you watch these, you'll start to understand the daily chatter of the market.

The dance between gold and the U.S. dollar is one of the most critical relationships to watch. Gold is priced in dollars, so when the dollar gets weaker, gold becomes cheaper for anyone holding other currencies. This often boosts demand and drives the price up. A strong dollar, on the other hand, usually has the opposite effect.

Here’s a quick breakdown of the major market movers:

| Factor | How It Typically Influences Gold | Real-World Example |

|---|---|---|

| Interest Rates | Higher rates make interest-bearing assets like bonds more attractive, potentially pulling money away from gold, which pays nothing. | When the Federal Reserve raises interest rates to combat inflation, holding gold becomes less appealing compared to earning a guaranteed return from a government bond. |

| U.S. Dollar Strength | A weaker dollar usually means a higher gold price, and a stronger dollar often means a lower one. | If the dollar falls against the euro, a buyer in Germany can suddenly afford more gold with the same amount of money, pushing up demand and the dollar price. |

| Geopolitical Instability | Wars, trade disputes, and political chaos create fear. In times of fear, investors flock to gold as a safe place to park their money. | During an international crisis, you'll often see investors sell stocks and rush into gold, causing its price to climb as a 'safe-haven' asset. |

Getting a handle on these dynamics is key for anyone trying to follow business insider's guide to market trends. Once you start connecting these dots, you’ll stop just watching the price of gold and start actually understanding it.

Choosing Your Path to Gold Investment

Deciding to add gold to your portfolio is one thing. Figuring out how to actually own it is a whole other puzzle. There isn't just one way to invest in gold; you've got several different paths to choose from, and each comes with its own rules, costs, and perks.

The best choice really boils down to what you're trying to achieve. Are you after the security of holding a physical asset? The ease of trading on a stock exchange? Or maybe you're looking for amplified returns through the mining industry? There’s no single "right" answer—just the one that fits your own strategy and comfort level. Let's walk through the main options.

Physical Gold Bullion and Coins

This is the classic, old-school way to own gold. When you buy physical gold, you're getting actual gold bars (bullion) or coins that you can hold in your hand. For many people, that tangible quality is the biggest appeal.

- Gold Bars: Also known as bullion, these come in all shapes and sizes, from a tiny one-gram wafer to the hefty 400-ounce bars you see in bank vaults. Generally, the bigger the bar, the lower the premium (the amount you pay over the gold's market price). This makes larger bars a very cost-effective way to stack pure gold.

- Gold Coins: Coins like the American Gold Eagle, Canadian Maple Leaf, and South African Krugerrand are minted by governments, guaranteeing their weight and purity. They usually have a slightly higher premium than bars, but they're instantly recognizable and easy to sell. Some even have a bit of collectible value on the side.

Holding physical gold gives you a sense of security that a line on a screen just can't match. The flip side? You have to figure out where to store it safely and how to insure it. These aren't minor details; they're essential for protecting your investment. If you're leaning this way, a resource like A Modern Guide to Investing in Gold Bullion can be incredibly helpful.

Gold Exchange-Traded Funds (ETFs)

What if you want to bet on gold's price without dealing with the hassle of storing bars and coins? That’s where Gold ETFs come in. Think of an ETF as a giant fund that buys and holds massive amounts of physical gold in high-security vaults. You simply buy shares of that fund on the stock market, just like you would with a company like Apple or Google.

The value of your shares tracks the price of gold almost perfectly. This makes ETFs incredibly liquid—you can buy or sell them in seconds whenever the market is open. Their convenience and low fees have made them a go-to choice for modern investors. A recent report from the World Gold Council highlighted this, noting that ETF demand was a key driver as total US gold demand surged by 140% to 679 tons—the highest level seen since 2020.

Gold Mining Stocks

Here's another indirect route: buying shares in the companies that dig gold out of the ground. It's a simple idea. When the price of gold goes up, mining companies stand to make more money, and their stock prices often follow suit.

This approach offers a unique kind of leverage.

If you pick the right mining company, your returns could actually outpace the rise in the gold price itself. On top of that, some mining stocks pay dividends, giving you an income stream that a bar of gold never will.

But be warned, this path comes with a whole different set of risks. You're not just betting on gold; you're betting on a business. That means you're exposed to everything from poor management and operational hiccups to political turmoil in the countries where they operate.

Comparing Your Gold Investment Options

To help you see the pros and cons at a glance, this table breaks down how the most popular gold investments stack up against each other. It’s a quick way to see which option might align best with your goals.

| Investment Type | Pros | Cons | Best For |

|---|---|---|---|

| Physical Gold | Tangible ownership, no counterparty risk, universally accepted store of value. | Requires secure storage and insurance, higher premiums, less liquid. | Investors who prioritize direct ownership and want a long-term hedge outside the financial system. |

| Gold ETFs | Highly liquid, low transaction costs, no storage concerns, easy to trade. | You don't own the physical gold, subject to management fees. | Investors seeking convenient, short-to-medium-term exposure to gold price movements. |

| Mining Stocks | Potential for high returns, possible dividend income, leverages gold price gains. | Higher risk than gold itself, exposed to company and market risks. | Investors with a higher risk tolerance seeking leveraged exposure to the gold sector. |

| Digital Gold | Easy to buy in small amounts, simple online storage, highly divisible. | Less regulated, counterparty risk with the provider, a newer and less tested asset class. | Tech-savvy investors who value convenience and want to own fractional gold without ETF fees. |

Choosing the right method is about matching the investment's characteristics to your own financial situation and what you hope to accomplish.

Ultimately, the price of gold comes down to the timeless tug-of-war between supply and demand. Each of these investment methods simply offers you a different seat at the table to participate in that market. If you're still building your foundation, our guide on https://everydaynext.com/investing-strategies-for-beginners/ is a great place to start.

Navigating Current Gold Market Trends

Knowing the history of gold is one thing, but making smart investments means understanding what’s driving the market right now. A few powerful forces are shaping gold’s story today, influencing its price and how it fits into the global economy. If you’re a gold investor, these are the trends you need to watch.

One of the biggest stories is the sheer volume of gold being bought by central banks. We're not talking about small tweaks to their balance sheets. These institutions are acquiring gold at a historic clip, signaling a major global shift to diversify their reserves away from the U.S. dollar.

This steady, large-scale buying creates a strong price floor for gold. Think about it: when the world’s biggest financial players are consistently stocking up, it’s a massive vote of confidence in gold's long-term stability.

Central Banks on a Gold Buying Spree

For years, central banks have been net buyers of gold, but what we've seen recently is a dramatic acceleration. This isn't a random occurrence. It's a calculated move to protect against geopolitical flare-ups, economic instability, and the very real risk of currency devaluation.

Countries like China and Poland are leading the charge, adding tons of gold to their vaults month after month. This is more than just financial housekeeping; it's a strategic play for greater economic independence and stability in a very uncertain world.

The message couldn't be clearer: when things get unpredictable, nations fall back on the oldest and most trusted form of money. This institutional demand is a fundamental pillar holding up the current gold market.

This sustained buying has had a huge impact. According to the World Gold Council, the trend helped push global gold demand to a record-breaking 5,002 metric tons—the highest level ever recorded. This happened even as prices were hitting new highs, which just goes to show how strong the appetite for gold really is. You can read more about this record demand on investing.com.

Gold Versus Bitcoin: The Modern Debate

You can’t talk about gold today without bringing up its digital cousin, Bitcoin. Often called "digital gold," Bitcoin has a few things in common with the yellow metal—most notably, a limited supply and its use as an alternative to traditional currencies. The debate over which one is the better store of value is one of the hottest topics in finance.

This table breaks down how they stack up:

| Feature | Gold | Bitcoin |

|---|---|---|

| History | A store of value for thousands of years. | A little over a decade old. |

| Tangibility | A physical asset you can hold in your hand. | Purely digital; exists only on a network. |

| Volatility | Relatively stable, with much lower volatility. | Famous for its extreme price swings. |

| Regulation | A highly regulated and established market. | The regulatory landscape is still evolving. |

| Use Case | Jewelry, industry, and investment. | Mostly a speculative asset and payment network. |

While Bitcoin has produced some incredible returns, its wild volatility and uncertain regulatory future make it a much riskier bet. Gold, by contrast, has a proven track record of preserving wealth through centuries of turmoil.

Many investors now see a place for both in their portfolio—gold for its reliable stability and Bitcoin for high-risk, high-reward speculation. Gold's steady performance in the face of ongoing economic headwinds remains a key draw for investors. To get a better sense of the economic climate, you might be interested in our inflation forecast for 2025.

Smart Steps for Every Gold Investor

Buying gold is just the first step. To truly make it work for you, you need a solid plan for what comes next. The practical side of things—like where you'll keep it, how it's taxed, and where it fits in your overall strategy—is what really protects your investment and makes sure it does its job.

These details aren't overly complicated, but getting them right is what separates a casual buyer from a serious, well-prepared investor.

Securing Your Physical Gold

If you've decided to buy physical gold, whether it's bars or coins, your first thought should be: "Where am I going to keep this?" You really have two main paths, each with its own pros and cons. The right choice depends on how much gold you have, your personal comfort level with risk, and how fast you might need to get your hands on it.

Home Storage: For a modest amount of gold, a high-quality, fireproof safe that’s bolted to the floor is a reasonable choice. You have instant access and total control. The downside? You're entirely responsible for its security, and your insurance company might charge you a higher premium.

Professional Vaults: If you’re holding a significant amount, using a third-party depository or even a bank's safe deposit box is a much safer bet. These places are built like fortresses and are fully insured, giving you genuine peace of mind. The trade-off is the annual storage fees and the fact that you can't just grab your gold on a whim.

Understanding Tax Implications

Here’s something that catches a lot of new gold investors off guard: gold isn't taxed like stocks or bonds. In many places, including the U.S., the tax authorities classify physical gold as a "collectible."

What does that mean for your wallet? If you hold gold for over a year and then sell it at a profit, your gain is taxed at the collectible capital gains rate, which can be as high as 28%. That’s a good deal higher than the typical long-term capital gains rates for most other investments.

It's crucial to bake these tax considerations into your plan from the very beginning. A quick chat with a tax advisor can save you from a nasty surprise when you eventually decide to sell.

Allocating Gold in Your Portfolio

So, the big question: how much gold should you actually own? There's no single magic number, but a long-standing rule of thumb from financial advisors is to allocate somewhere between 5% and 10% of your total portfolio to gold.

This range is seen as the sweet spot. It's enough to provide a real hedge against inflation or a stock market downturn, but not so much that you're over-exposed to the price swings of a single commodity. For most people, gold isn't about hitting home runs; it's about playing defense.

This simple table helps visualize why that 5-10% range is so popular:

| Portfolio Allocation | Primary Goal | Risk Profile | Potential Impact |

|---|---|---|---|

| Below 5% | Minimal Hedging | Low Exposure | Might not offer much protection when you really need it. |

| 5% – 10% | Balanced Diversification | Moderate Exposure | The standard approach for balancing safety and growth potential. |

| Above 10% | Strong Hedge | High Exposure | Can limit your portfolio's growth and makes you highly dependent on gold's performance. |

Think of that allocation as your portfolio's insurance policy. It's there to protect you when things get rocky, allowing the rest of your investments to focus on growth.

Putting It All Together: Your Gold Investment Game Plan

Alright, we've covered a lot of ground—from gold's history to the nitty-gritty of ETFs and bullion. But knowledge is only half the battle. Now it’s time to take what you've learned and build a smart, actionable strategy.

The first step is the most important: get clear on your "why." Before you even think about buying, ask yourself what you want gold to do for your portfolio. Are you looking for a long-term anchor to preserve wealth? A hedge to protect you when the stock market gets choppy? Or are you simply trying to diversify your assets? Your answer here will shape every other decision you make.

A Quick Checklist Before You Buy

To make this simple, think of it as a step-by-step process. Following this checklist will help you move from planning to ownership without missing any crucial details.

- Set Your Budget: Decide exactly how much you're comfortable investing. Most financial experts recommend allocating around 5-10% of your total portfolio to gold. This gives you meaningful protection without going overboard.

- Pick Your Gold: Based on your goals, choose the right type of investment for you. Will it be physical coins you can hold, a low-fee ETF you can trade like a stock, or shares in a mining company?

- Find a Reputable Seller: This is a big one. If you're buying physical gold, do your homework on established bullion dealers. Look for transparent pricing and a solid track record. For ETFs or stocks, you'll need a reliable brokerage account.

- Make the Purchase: Pull the trigger. When you place your order, make sure you know the current spot price and are clear on any extra costs, like premiums or brokerage fees.

- Secure Your Asset: If you bought physical gold, this is your immediate next step. Figure out storage right away. That could mean a high-quality safe at home or space in a professional, third-party vault.

What's Next?

Think of this guide as your starting point. The gold market is always moving, and staying informed is the key to making smart decisions over the long haul. If you're just getting started with building your portfolio, our guide on how to invest money for beginners is a great next read.

Key Takeaway: The most successful gold investors play the long game. They aren't trying to time the market or chase quick profits. Instead, they build their position patiently and treat gold as a permanent, stabilizing force in their financial strategy.

By following a clear plan, you're doing more than just buying a shiny metal—you're making a strategic decision to strengthen your financial future.

Frequently Asked Questions About Gold Investing

Diving into gold can bring up a lot of questions. Whether you're just starting to think about it or you've been investing for years, there are always new things to consider. Here are answers to ten of the most common questions people ask.

1. How much of my portfolio should I allocate to gold?

Financial advisors commonly recommend allocating 5% to 10% of your portfolio to gold. This amount is generally considered sufficient to provide diversification benefits and a hedge against economic downturns without overexposing your portfolio to the price swings of a single commodity.

2. Is physical gold or a gold ETF better for a beginner?

For most beginners, a Gold ETF is the more accessible option. ETFs are bought and sold through a standard brokerage account just like stocks, have low transaction costs, and eliminate the need to worry about storage and insurance. Physical gold offers the benefit of direct ownership but comes with higher upfront costs (premiums) and the responsibility of securing the asset.

3. What are the biggest risks of investing in gold?

The main risks include price volatility, as gold's value can fluctuate with economic data and market sentiment. Gold is a non-yielding asset, meaning it pays no dividends or interest, so your return depends entirely on price appreciation. For physical gold, there is also the risk of theft and the ongoing costs of storage and insurance.

4. How can I be sure the physical gold I buy is authentic?

Always buy from reputable and well-established dealers. Authentic bullion coins and bars are stamped with their weight, purity (e.g., .9999 fine), and the name of the mint or refiner. Reputable sellers can verify authenticity and will often provide an assay certificate. Be wary of deals that seem too good to be true.

5. Are gold coins a better investment than gold bars?

It depends on your goals. Gold bars typically have lower premiums over the spot price, making them a more cost-effective way to accumulate pure gold weight. Gold coins, such as American Eagles or Canadian Maple Leafs, have slightly higher premiums but are easily recognizable, easier to sell in smaller quantities, and may have numismatic (collectible) value.

6. What is the difference between the "spot price" and the "premium"?

The spot price is the current market price for one troy ounce of gold that is ready for immediate delivery. It fluctuates throughout the day. The premium is an additional amount charged by a dealer over the spot price to cover the costs of fabrication, distribution, and their profit margin. You will always pay the spot price plus a premium when buying physical gold.

7. How do I sell my physical gold?

You can sell physical gold to most reputable bullion dealers, coin shops, or precious metal exchanges. They will typically offer to buy it at or slightly below the current spot price. It's a good practice to get quotes from several different buyers to ensure you are receiving a competitive price.

8. Does gold pay dividends or interest?

No. Unlike stocks that may pay dividends or bonds that pay interest, gold is a tangible asset that does not generate any income. Its investment return is based solely on price appreciation over time. This makes it a pure "store of value" rather than an income-producing investment.

9. Is gold a good investment for retirement?

Gold can be a valuable component of a retirement portfolio. Its historical stability and role as a hedge against inflation and market volatility can help preserve wealth over the long term. It provides balance to a portfolio that also contains growth-oriented assets like stocks, helping to smooth out returns, especially during economic uncertainty.

10. How do I avoid common gold investment scams?

Be skeptical of unsolicited offers and high-pressure sales tactics that promise "guaranteed" or unusually high returns. Stick to well-known dealers with a physical presence and a long history of positive customer reviews. Avoid sellers pushing obscure "rare" coins with exorbitant premiums. Always research a dealer thoroughly before making a purchase.

At Everyday Next, we're committed to providing clear, actionable insights to help you build a stronger financial future. Explore more of our guides on wealth, tech, and personal growth at https://everydaynext.com.

Previous Post

Next Post