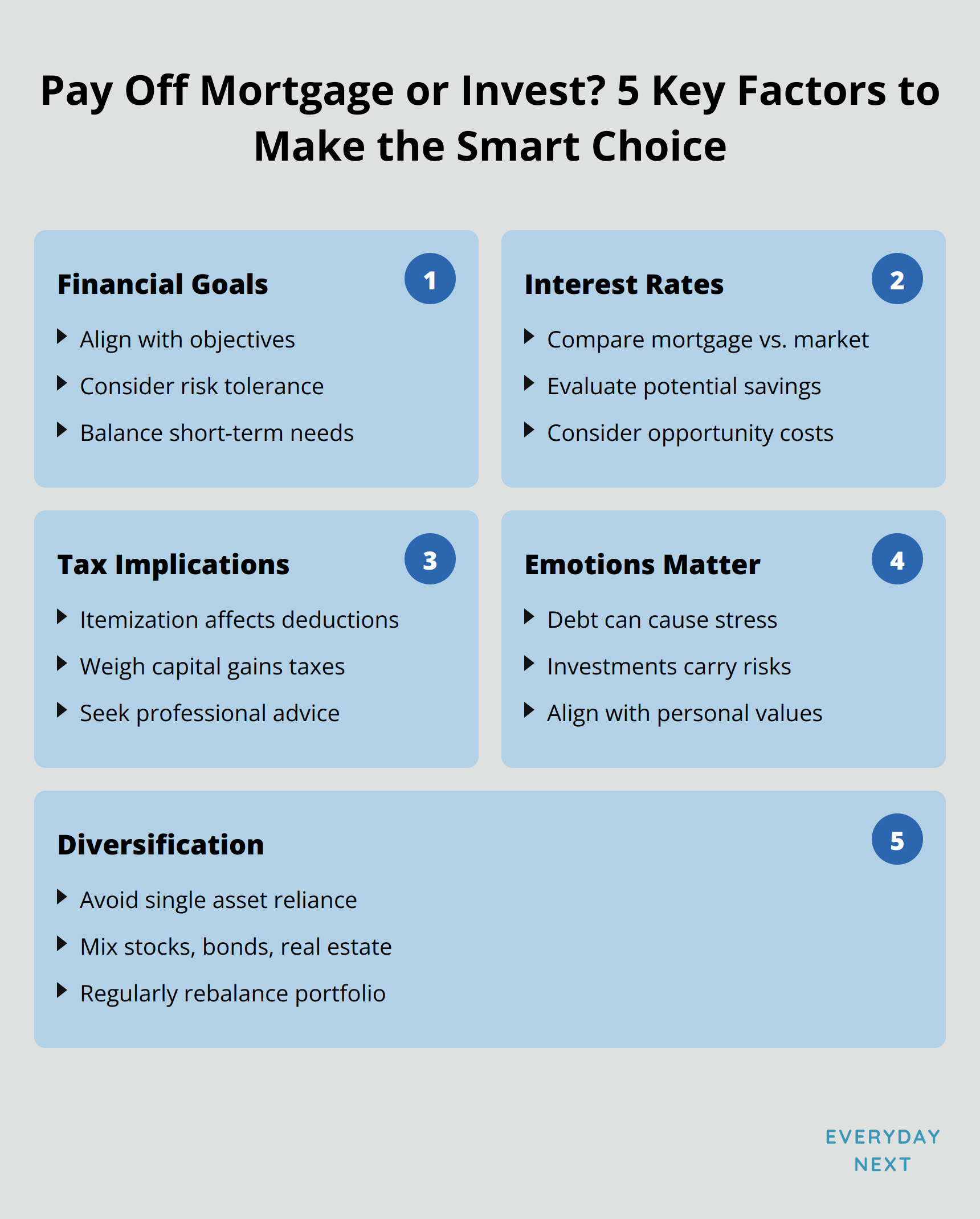

Pay Off Mortgage or Invest? 5 Key Factors to Make the Smart Choice

Table of Contents

At Everyday Next, we understand your dilemma. You’re torn between two options in this financial derby: Pay Off Mortgage or Invest? This decision could reshape the entire skyline of your financial future. It’s essential to weigh your options carefully when considering whether to Pay Off Mortgage or Invest? and how that choice influences your long-term financial health. Ultimately, the question remains: should you Pay Off Mortgage or Invest? Your answer will depend on your unique financial landscape and personal goals.

In this post, we’ll unpack five key factors to help you decide whether to rid yourself of mortgage debt early or invest. We’re diving deep into the intricacies of each path, equipping you with insights tailored to your unique financial dreams and circumstances surrounding the question: Pay Off Mortgage or Invest?

Consider how your decision to Pay Off Mortgage or Invest? influences your overall financial strategy.

As you ponder this decision, reflect on how the choice to Pay Off Mortgage or Invest? aligns with your financial goals and risk tolerance.

As you navigate your financial journey, remember to revisit the question: Pay Off Mortgage or Invest?

Understanding your financial landscape will help you answer the question: should I Pay Off Mortgage or Invest?

Your decision to Pay Off Mortgage or Invest? should align with your overall financial vision.

Are you leaning more towards choosing to Pay Off Mortgage or Invest?? Reflect on your motivations.

Weighing the decision to Pay Off Mortgage or Invest? involves considering the current market conditions and your personal circumstances.

Ultimately, thinking through the implications of whether to Pay Off Mortgage or Invest? can lead to a more secure financial future.

Your choice to Pay Off Mortgage or Invest? isn’t just a financial decision; it reflects your personal priorities and situation, which can change over time.

1. Financial Goals Shape Your Mortgage vs. Investment Strategy

Your financial goals are basically your coordinates in this financial scavenger hunt. You’re stuck in a mortgage vs. investment wrestling match, and you’d better make sure your long-term objectives have referee whistling them in the right direction. Want to pack up the 9-to-5 dance early? Get aggressive with investing like it’s your last day at an all-you-can-eat buffet. But if dreaming of a mortgage-free life by 50 gets you misty-eyed, throw that extra coin at the mortgage beast, and call it a day. The decision to Pay Off Mortgage or Invest? hinges on your risk tolerance… it’s not just a Wall Street buzzword. Are you the type who can stomach a roller-coaster market? Or does the mere thought have you reaching for the Pepcid?

Ultimately, the question remains: should you Pay Off Mortgage or Invest? Your answer will depend on your unique financial landscape and personal goals.

Understanding whether to Pay Off Mortgage or Invest? can greatly impact your financial journey.

Balancing short-term and long-term needs can be challenging. If you have children approaching college, liquidity becomes essential. Conversely, if you’re planning to stay in your current home for an extended period, reducing your mortgage interest might feel rewarding. A Bankrate survey revealed that over half of Americans are lagging behind in retirement savings (don’t join this club). Your decision should not be a simple coin toss; it should be a strategic move toward your financial vision. Here’s your decision-making checklist:

- Your retirement timeline and goals (stick to the plan, don’t wing it)

- Your risk tolerance and investment preferences (adrenaline junkie or safety fan?)

- Your short-term financial needs (e.g., education expenses, home repairs)

- Your long-term financial dreams (e.g., early retirement, wealth building)

- Your retirement timeline and goals (stick to the plan, don’t wing it)

- Your risk tolerance and investment preferences (adrenaline junkie or a safety fan?)

- Your short-term financial needs (e.g., education expenses, home repairs-adulting, basically)

- Your long-term financial dreams (e.g., early retirement, wealth building-the spotlight of your future Netflix doc)

All these considerations, and don’t forget about interest rates… those unsung hero-villains of your financial plot line.

Understanding whether to Pay Off Mortgage or Invest? can greatly impact your financial journey, helping to clarify your long-term strategy.

Choosing whether to Pay Off Mortgage or Invest? requires understanding both immediate and long-term financial impacts.

Your assessment should include whether you prefer to Pay Off Mortgage or Invest? and how interest rates affect that choice.

Consider the broader implications of deciding to Pay Off Mortgage or Invest? for your financial future.

Ask yourself: should I Pay Off Mortgage or Invest? What aligns better with my financial goals?

2. Interest Rates: The Tipping Point in Your Decision

Interest rates – they’re the fulcrum in the age-old should-I-pay-off-my-mortgage-or-invest debate. So, here we are, February 2025. We’ve watched the 30-year fixed-rate float between 6% and 7% for over two years, while the S&P 500’s been spinning out an average annual return of 10.13% since 1957. Tempting to throw your spare cash at the market, right? But hold on. Markets – have mood swings; that 10.13% is more of a rollercoaster than a guarantee, while your mortgage rate is more like a cruise ship – steady.

To assess your situation, calculate the total interest of your mortgage and compare it with potential investment returns. An amortization calculator can help illustrate how much you could save with extra mortgage payments. Consider opportunity costs; putting an additional $500 monthly toward your mortgage may prevent you from seizing investment opportunities. However, if your mortgage interest rate exceeds 7%, aggressively paying down that mortgage could be advantageous.

- Your current mortgage interest rate

- Historical and what-the-future-might-hold market returns

- Savings from those extra mortgage payments

- The opportunity cost of skipping investments

Interest rates are a crucial factor in the age-old debate: should I pay off my mortgage or invest? As of February 2025, we’ve seen the 30-year fixed-rate mortgage fluctuate between 6% and 7% for over two years, while the S&P 500 has averaged an annual return of 10.13% since 1957. It’s tempting to invest your extra cash, but remember that markets can be volatile; that 10.13% is not guaranteed.

3. Tax Implications of Mortgage Payoff vs Investing

Your emotional comfort level will also influence whether you choose to Pay Off Mortgage or Invest?.

When weighing your options, don’t overlook taxes. These implications play a significant role in your decision to pay off your mortgage or invest. Mortgage interest deductions are beneficial only if you itemize. For 2025, the standard deduction is $15,000 for singles and $30,000 for married couples filing jointly. Many homeowners no longer benefit from itemization. On the flip side, long-term capital gains are taxed at 0%, 15%, or 20%, depending on your income, while short-term gains are taxed at your regular income rate.

Take a step back and see the full picture-it’s all about tax efficiency. High tax bracket peeps might actually shave off thousands with that mortgage interest deduction. But wait, there’s more. Stuff like Roth IRAs might offer tax-deductible contributions that outshine mortgage interest deductions over time. Getting the professionals involved-yep, we’re talking tax pros-can help you crunch the numbers on the after-tax costs of hanging onto the mortgage versus the potential after-tax returns from investments. This number-fest is crucial for making a decision that aligns with your wallet and tax situation. Now, let’s segue into how the heart-yep, those pesky emotions-plays into this whole financial decision-making saga.

Understanding the full financial picture is crucial. High-income earners might save significantly with mortgage interest deductions, while others may find that investment vehicles like Roth IRAs offer more advantageous tax benefits in the long run. Consulting with tax professionals can provide insights into the after-tax costs of maintaining your mortgage versus potential after-tax returns from investments.

Financial decisions are deeply personal. Paying off your mortgage can relieve significant stress. However, investing carries its own risks, particularly during market fluctuations, which can impact your mental well-being. Recent surveys indicate that a large percentage of Americans are concerned about market volatility, even as they invest.

Before deciding whether to Pay Off Mortgage or Invest?, consider how each option aligns with your overall financial aspirations.

- Your comfort with carrying debt

- Your appetite for investment risk

- Your overall financial aspirations

- Your emotional response to financial decision-making

Trust your gut. If debt’s keeping you tossing and turning at night, maybe scratching off that mortgage is your ticket to peace. But fear-not the best advisor. Sure, paying off debt feels great, but what about those gains you could be missing out on? (Remember, the S&P 500 has a history of its own roller-coaster returns.) And don’t forget about values. Some folks cherish that sweet, sweet financial freedom over paper wealth. Others? They’ll ride the debt wave if it means their nest egg might swell. No one-size-fits-all here, folks. Sit back and really think-what hits home for you? Weigh these factors:

- Your comfort with carrying debt

- Your appetite for risk in investments

- Your big-picture financial dreams

- How you emotionally handle financial decisions

As you’re juggling these emotional factors-don’t lose sight of something crucial. Concentrating all your wealth in one bucket? Could be a killer. Time to dive into diversification… next on the docket.

5. Diversification Protects Your Financial Future

Consolidating all your wealth into a single investment is risky. While real estate can be a solid investment, it’s wise to diversify. The S&P 500 has historically outperformed real estate, averaging a 10.13% annual return since 1957, whereas home values have increased by only 3.8% annually since 1991. This highlights the importance of spreading your investments across various asset classes.

Paying off that mortgage – it feels fantastic, no doubt. But don’t let that high come at the expense of other potentially more lucrative investments. That extra cash? It could work harder for you if invested in a buffet of stocks, bonds, and maybe some alternative investments like REITs or crowdfunding platforms. Diversification reduces risk by betting on different horses across financial instruments, industries, and other categories. Remember the 2008 housing debacle? Those who had all their chips on homes – ouch – suffered big losses, while diversified folks had a much easier ride.

Reflect on your priorities when considering the choice to Pay Off Mortgage or Invest?, and how this aligns with your overall financial strategy.

Many find success in balancing the decision to Pay Off Mortgage or Invest? by analyzing their financial priorities carefully and seeking professional advice.

Paying off your mortgage feels great, but don’t let that satisfaction stop you from pursuing potentially more rewarding investments. Consider investing your surplus cash in a variety of assets, including stocks, bonds, and alternative investments such as REITs or crowdfunding. Diversification helps reduce risk by distributing investments across different sectors and asset types.

- Invest in a mix of stocks, bonds, and real estate

- Think about alternative investments like REITs or crowdfunding platforms

- Give your portfolio a regular health check – rebalance to keep your asset allocation on point

Reflect on your priorities when considering the choice to Pay Off Mortgage or Invest?, and how this aligns with your overall financial strategy.

Many find success in balancing the decision to Pay Off Mortgage or Invest? by analyzing their financial priorities carefully.

Having explored the fundamentals of diversification, let’s wrap up with actionable insights to empower your financial decisions.

Final Thoughts

As you consider whether to pay off your mortgage or invest, remember that your financial goals, interest rate conditions, tax implications, and emotional factors all play critical roles in your decision-making process. Weigh the pros and cons carefully and remember the importance of peace of mind in your financial journey.

Start by clarifying your financial priorities. Assess your current situation before making decisions. Use online calculators or spreadsheets to project outcomes between mortgage payoff and investment strategies. If necessary, consult with a financial professional for personalized guidance.

Consider a mixed approach; many individuals pay down debt while simultaneously investing. At Everyday Next, we’re prepared to provide tools and resources to help you confidently navigate your path to financial security.

Related Posts

Previous Post

Next Post